When the residents of Bedford Falls, New York, panic and want their money from the bank in “It’s a Wonderful Life,” Jimmy Stewart explains that cash isn’t piled in the safe.

“Your money’s in Joe’s house, and a hundred others,” he tells his customers. “You’re lending them the money to build and then they’re going to pay it back to you the best they can.”

That neighborly spirit is the core concept of how Alabama’s 89 credit unions do business, a spokesperson says.

In that movie, “how they started was through trust and wanting to help each other,” says Michelle Roth, vice president of advocacy for the League of Credit Unions.

The league represents institutions in Florida, Alabama, Georgia and Virginia. Roth’s responsibility from Montgomery is to watch legislation affecting credit unions and their members in Alabama.

“The whole mission of credit unions is helping people,” she says.

While worth billions today, in most cases Alabama’s credit unions had very humble beginnings.

Around the time of the Depression, “many working families really couldn’t get these loans they perhaps might have needed from a traditional bank,” Roth explains.

President Franklin Roosevelt signed the Federal Credit Union Act of 1934 to help establish credit options for citizens during the Depression. The idea was to create member-owned institutions that could offer low-cost credit. The first credit union in America opened in 1909 in New Hampshire. A new National Credit Union Administration formed in 1970 to supervise operations.

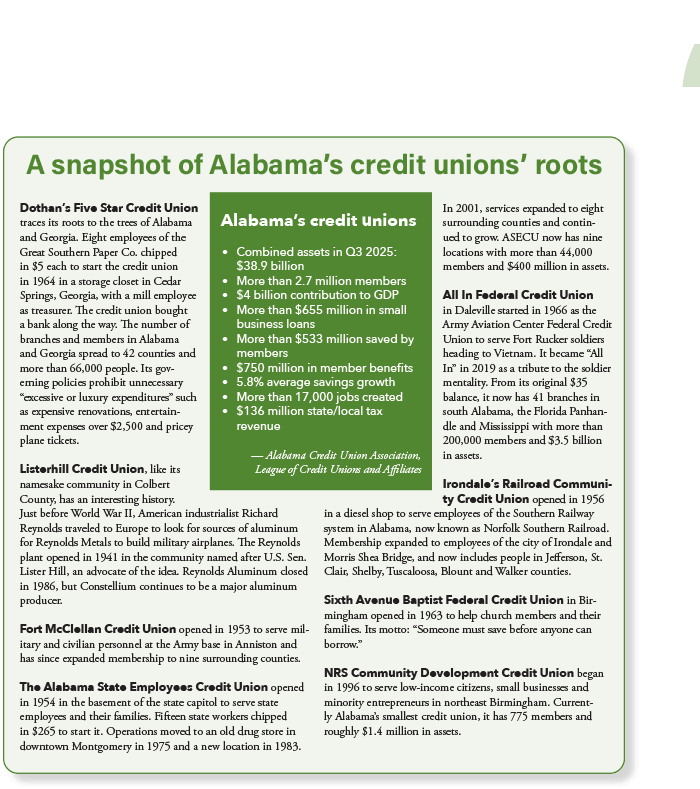

Airplane mechanics, Vietnam soldiers, state employees and railroad workers literally pitched in money from their precious paychecks to get Alabama’s various credit unions started. People with the same livelihoods — such as teaching or working in a sock factory — created cooperatives, pooled their funds and crossed their fingers. In Montgomery, Maxwell Air Force Base workers combined resources. University of Alabama at Birmingham employees started Legacy. Gadsden teachers were behind Emblem. In 1936, Tennessee Valley Authority employees created what is now TVA Community.

Redstone Federal Credit Union in Huntsville is the biggest of Alabama’s credit unions in terms of assets. In November 1951, 11 Redstone Arsenal employees put $5 each in a shoebox, and membership swelled through the years as the area’s needs grew. Now celebrating its 75th anniversary, RFCU operates 30 branches. Assets of more than $8 billion and 650,000 members around the world make it the nation’s 19th largest credit union.

“Created to provide financial services to those members of modest means, credit unions may be the only place some people can go to get free financial counseling, flexible loan products and better rates on those products,” says RFCU President Joe Newberry.

Redstone defines success by taking care of its members and giving back to the community, Newberry says. RFCU provided more than $900,000 in sponsorships to non-profits last year. Its Community Impact Grant Program awarded $230,000 to support philanthropic work in north Alabama.

“Improving the financial well-being of our members and communities is our mission,” Newberry adds. “We do that in many ways, including awarding college scholarships, providing financial counseling and by volunteering and serving with non-profits in critical areas. We also do that with great rates, fewer fees and more product offerings.”

Redstone’s field of membership was initially open to just military and civilian employees of Redstone Arsenal, defense contractors and their immediate families. However, as Redstone’s marketing extended, more members joined and by 1957 totaled 6,000.

Credit union advocates say those institutions are in a position to understand an individual’s credit history, respond directly to community needs and provide flexible loans at competitive rates.

Another distinction of credit unions is that “decisions are made locally by a volunteer board elected by members,” Roth says, allowing them to be responsive to their local communities.

“The core principles that guide Listerhill are deeply rooted in the credit union philosophy, emphasizing member-centric values over profit-driven motives,” says Ashley Mobley, Listerhill’s vice president of compliance in Muscle Shoals.

“Each member is an owner with a voice in the governance of the credit union,” says Mobley. “Decisions are made in the best interest of the membership. Profits are reinvested into the credit union, allowing Listerhill to offer competitive interest rates on loans and higher rates on deposit accounts, along with lower fees.”

Avadian Credit Union began in 1934 as Alabama Telco to serve telephone company employees and their families.

“While we’re proud to offer great rates and fewer fees, we feel that what truly sets us apart is service — service to the members who have entrusted us with helping them manage their financial lives, and service to the communities around us,” says Vice President of Marketing Ashley Wilbanks.

Avadian now has more than 85,000 members from Dothan to Huntsville.

While they appear to operate much like banks, credit unions have different guidelines and overseers.

“We have a federal charter with clear rules that define how we can operate safely and responsibly,” Roth says. The Federal Deposit Insurance Corp. insures bank assets. The National Credit Union Association insures non-profit credit unions.

Forty Alabama credit unions operate under federal charters and 49 with state charters. The NCUA oversees all federal credit unions, whether they are federally or state chartered. The Alabama Credit Union Association oversees only state-chartered credit unions. Roth explains that a federal credit union can change to a community and state charter but must go through the NCUA approval process.

The ACUA has updated its regulations to align more with NCUA guidelines in addressing virtual meetings, loans to other credit unions and branches out of state.

Credit union advocates like to note that because they are community-based, they often get involved in addressing issues they see locally. Alabama’s credit unions helped pass legislation requiring financial literacy education in Alabama’s classrooms.

Families need to “understand financial awareness so that they don’t become victims of predatory lending and the crazy interest in payday loans,” Roth says.

“We have so much in common with community banks about serving the areas that we’re in,” she says. “There’s so much that we agree on in wanting to help. We have that same view, and we all want to give back to community.

“The decisions for your money are made based on giving back to you and the other members rather than to stockholders.”

Not operating under the same rules as commercial banks hinders them in one area, Roth notes. A “frustrating” bit of state legislation excludes them from competition for some local business. The Alabama Security for Alabama Funds Enhancement, or SAFE act, says public municipalities, utilities and school systems must do business with an FDIC-insured institution – meaning a bank.

For example, she says, “there’s not a single bank in Coosa County,” but Coosa Pines Federal Credit Union is there to serve the area.

Just as credit unions want to help the community, they try to be there for each other, too. When one North Alabama credit union was hacked and lost its phone service, another offered use of their phones.

“You’re not going to see that in other industries that are so highly competitive,” says Roth.

As a whole, the state’s credit unions have an issue that their founders never envisioned – keeping their members’ nest eggs safe from online thieves.

“One of the top absolute priorities for our credit unions is fraud protection, especially for elder financial exploitation,” Roth says. “They’re getting taken advantage of in just horrible ways.”

As the state’s credit unions continue to add members and grow assets, they intend to keep the founders’ neighborly spirit as the backbone of their operations.

“We continue to grow, but we also want to stay true to why we were created in the first place,” says Roth.

Deborah Storey is a Huntsville-based freelance contributor to Business Alabama.

This article appears in the March 2026 issue of Business Alabama.